Vikas Life Quarterly Earnings: Strong Revenue Jump, But Profitability Still Under Pressure

Have you been tracking small-cap chemical stocks lately? If yes, then you might have noticed how sharply Vikas Lifecare Ltd. is reacting to its quarterly numbers.

In the latest Q4 FY25-26 results, the company surprised the market with a strong jump in revenue. But profitability is still under pressure at the same time. That mix of gains and losses is exactly what has investors inquisitive and concerned.

In this post, let’s break down the current earnings in a simple approach and grasp what these data are truly saying us about the stock’s financial health.

About Vikas Life Sciences:

Vikas Lifecare Ltd is in the chemicals business, with specialisation in specialised chemicals and allied business divisions. Earnings are erratic, as with many small-cap chemical companies, due to raw material costs, margins and demand cycles.

Latest quarterly results (Q4 FY 25/26) The firm presented their earnings report on June 24, 2026.

Here’s what the figures look like:

Key points

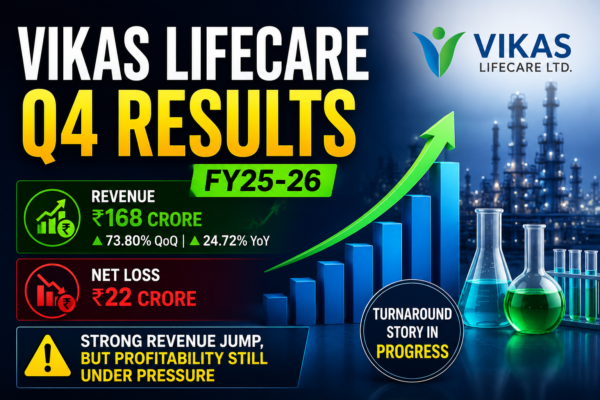

Revenue: Rs 168 crore

QoQ Growth: +73.80%

YoY Growth: +24.72% (t)

Gross Profit: -₹27 cr

Net Profit: -₹22 crore

Strong top-line growth did not prevent the company from being in loss territory.

What stands out from the earnings

1. Revenue Momentum Ramps Up

Vikas Life has posted a strong revenue gain this quarter. A 73.8% QoQ growth definitely indicates improving business activity and stronger demand flow.

But the growth has not turned into profits.

2. Ongoing losses

But despite the revenue growth, the company posted a net loss of Rs 22 crore.

QoQ losses slightly down

But still pressure on YoY performance

Cost structure Margins are still negative

That indicates the business is still in turnaround mode, not a constant time when it earns money.

3. Profit Trend Volatility Over Quarters

Looking back at historical performance, earnings have been quite erratic:

Best quarter earnings: Up to ₹11 crore (Jun ’23)

Worst losses: -₹26 crore (Mar ’23)

Recent quarters: Mostly negative

This volatility shows that earnings visibility is still restricted.

Cost Structure: What’s on the Line?

Look closely, and you will see the pressure coming from the following:

Raw material & purchase cost: High, Inconsistent

Other expenses: Elevated to ₹31 crore in last quarter

Operating leverage: Still not working in favour

“We are seeing revenue growth, but cost control is not yet fully in place.

EPS Summary

Latest EPS: ₹0.22 (excluding unusual items)

Previous quarters: Mostly negative EPS

Trend: Slow recovery, but fragile EPS recovery depends on ongoing profitability in coming quarters.

What Investors Should Look For Next

Key triggers ahead:

1. Margins Improvement

Growing revenue will not assist unless margins go positive.

2. Fluctuations in Raw Material Costs

Chemical firms rely greatly on input cost stability.

3. Steady Profitability

A few profitable quarters in succession can do wonders to market sentiment.

4. Management Guidance

Future commentary on demand outlook will be crucial.

Conclusion

To sum it up, Vikas Lifecare Ltd. is clearly showing strong revenue traction, but profitability is still lagging behind.

The company is growing fast, but it is not yet growing efficiently.

If management manages to control costs and sustain revenue momentum, the stock could enter a much stronger phase in the coming quarters. Until then, investors should treat this as a turnaround story in progress rather than a fully stable growth stock.

Keep an eye on the next few earnings reports; they will decide whether this momentum turns into real long-term value creation or remains inconsistent.

Read More –

FAQs

Q1. How Vikas Lifecare performed on revenue front this quarter?

The company posted strong operational performance with solid sales increase of ₹168 crore for Q4 FY25-26. This implies a good growth of approx. 73.8% on QoQ basis and approx. 24.7% on YoY basis. This means increasing activity of the company and revival of demand.

Q2. Revenue growth is accelerating, but is the company making money?

No, despite the large rise in income, Vikas Lifecare continued to incur losses. The company has posted a net loss of over Rs 22 crore indicating that the higher sales have not yet turned into profitability.

Q3. What is the pattern in earnings telling you about the company?

Earnings pattern is inconsistent. Previous quarters have generated momentary profits but following results have been largely negative. “It shows the company is still in a turnaround stage.

Q4. Why is profitability still under pressure despite strong revenue growth?

The main pressure comes from high input costs and high operational expenditures. Revenue growth is not converting to profits as raw material costs, and other factors, continue to weigh on margins.

Q5. How consistent has the company’s earnings record been?

Profitability has been very unpredictable. The company had recorded earnings as high as Rs 11 crore in certain preceding quarters and losses as high as Rs 26 crore in other quarters. This implies that earnings visibility is not uniform.

Q6. What does EPS tell us about the company’s performance?

Latest EPS is approx Rs0.22 (excluding one offs) indicating slight improvement. But most prior quarters had negative EPS, indicating recovery remains fragile.

Q7. What are the key factors investors need to be looking at going forward?

Investors should watch for margin improvement, steady raw material costs, stable profitability over the next few quarters and management’s commentary on future demand and cost control.”

Q8. Is Vikas Lifecare stock a stable growth stock now?

Not quite yet. Revenue is growing strongly, but uneven profitability and margin pressures imply the company remains a turnaround tale, not a steady long-term growth stock.

For More Information: Download Stockyaari App Now

Standard warning: “Investment in securities market are subject to market risks. Read all the related documents carefully before investing.” Disclaimers: a. “Registration granted by SEBI, enlistment as RA with Exchange and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.” b. “The securities quoted are for illustration only and are not recommendatory.”

This analysis is for informational purposes only. Please consult a SEBI-registered financial advisor before investing.

– Chandan Pathak

Equity Research Analyst, StockYaari